Glossary of Terms

Glossary of Terms

TABLE OF CONTENTS

CPA – Certified Public Accountant

Home Values (Residential Property)

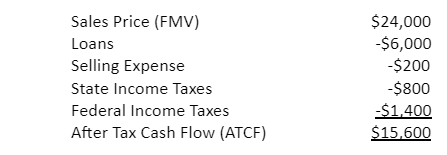

Simply put, it is the amount of real cash in your pocket from the receipt of cash from the sale of an asset. It is the true net amount after paying off all loans outstanding, all costs associated with the sale, and all income taxes incurred.

For example, I have 100 Shares of XYZ stock, which has a fair market value (FMV) of $24,000. I owe $6,000 in loans against it, fees to sell the stock come to $200, and I incur $800 in State Income Taxes and $1,400 in Federal Income Taxes. My resulting after-tax cash flow (ATCF) is $15,600

Compare this amount to Equity below.

The valuation of your vehicle. Auto values can be estimated by using online services, getting value estimates from your local dealership, CAR MAX, or banker.

Online sites include:

www.edmunds.com/used-cars-for-sale/

www.facebook.com (Marketplace)

Cost basis in general is what you originally paid for an asset. If you acquired an asset other than by purchase, for example as a gift, inheritance, in trade, etc., special rules apply to compute the cost basis. In addition your cost basis can increase over time (improvements, dividend reinvestment, etc.) or decrease (depreciation, return of capital etc.). It is recommended you consult with a tax professional to Determine your cost basis.

CPA – Certified Public Accountant

CPA’s are state licensed accountants who can provide financial expertise in the many aspects that can impact your divorce. CPA’s can have specialization, extensive training, advanced college degrees and experience in the areas of Divorce Issues, such as Taxation, Business Valuation, Financial Statement Audit and Review, Forensics, Pension and Profit Sharing, Partnerships, Corporations, and more. It is important, based on your need, facts, and circumstances of your divorce, to consult with the best accounting firm and individuals to make sure your specific divorce issues and your interests are properly addressed.

- Federal Long Term Capital Gains Tax Rate (Fed LTCG Rate)

Currently the Federal Tax laws provide a more favorable income tax rate for taxable capital assets held more than one year. In Divorce|Split you can enter that rate applicable for you. When computing estimated income taxes on taxable assets held more than one year this rate will be applied to the gain realized on a potential sale.

- State Long Term Capital Gains Tax Rate (State LTCG Rate)

If your State has a long term capital gains rate like the Federal LTCG, you can enter that into Divorce|Split Settings. If in your State the tax on capital gains is treated like all other income, then you enter the State income tax rate you will most likely pay.

- Federal income Tax Rate (Fed Income Tax Rate)

You can enter in Divorce|Split Settings the most likely average federal income tax rate to be applied to all income including capital assets held for less than a year (Short Term Capital Gains).

- State Income Tax Rate

You can enter in Divorce|Split Settings the most likely average State income tax rate on all income, including capital assets held for less than a year (Short Term Capital Gains) you will most likely pay.

- Commissions on Real Estate Sales (Commission on RE)

Usually when you sell real property a brokerage commission is paid by the seller and this payment reduces the actual cash you will realize from the sale. When utilizing the After-Tax Cash Flow (ATCF) scenarios provided in the Premium or higher subscription, you have a choice of: (1) entering a typical rate of commission to be used on all real property sales along with the ability to make adjustments on a property-by-property basis or (2) leave it blank and manually enter the necessary adjustment on each property sale.

- Closing Costs Impacting Real Estate Sales (Closing Costs RE)

There are several typical closing costs incurred when selling real property. These can include but are not limited to title costs, recording fees, title insurance policy, escrow fees, notary fees, document preparation fees, wire fees, prorations for property taxes, fire insurance etc. You can simply use a percentage of sales price to estimate the impact on the sale and the resulting amount of gain subject to taxes.

- Federal Long Term Holding Period (Fed LTCG Holding Days)

The number of days one must hold a capital asset before selling to qualify for the federal long term capital gains rate.

- State Long Term Holding Period (State LTCG Holding Days)

The number of days one must hold a capital asset before selling to qualify for the State long term capital gains rate.

- Married and Single Exclusion Limit (Married Excl Limit, Single Excl Limit)

Currently the Federal tax laws, after having met their various requirements, allow on the sale of a taxpayer's personal residence an exclusion of the first $500,000 (married) or $250,000 (single) of gain realized on its sale.

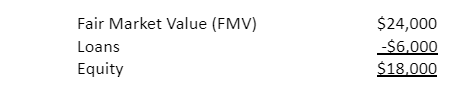

Equity is fair market value of an asset less the liabilities attached to that asset.

For example, I have 100 shares of XYZ stock with a fair market value of $24,000 but I owe the bank $6,000 so my equity is $18,000.

Compare to After-Tax Cash Flow above.

Home Values (Residential Property)

A Home’s value, or current estimated fair market value, can be provided by a local real estate broker or agent usually at no charge. Local multiple listing services have current listings and historical information on prior sales. Local real estate appraisals for a fee can appraise your property.

Recent sales and current listing of homes in your neighborhood can be found online from several sources including:

Talking with a few local Realtors, Brokers, or Agents in addition to doing your own research to understand your local market and evaluate your home usually can result in a fair estimate of current value.

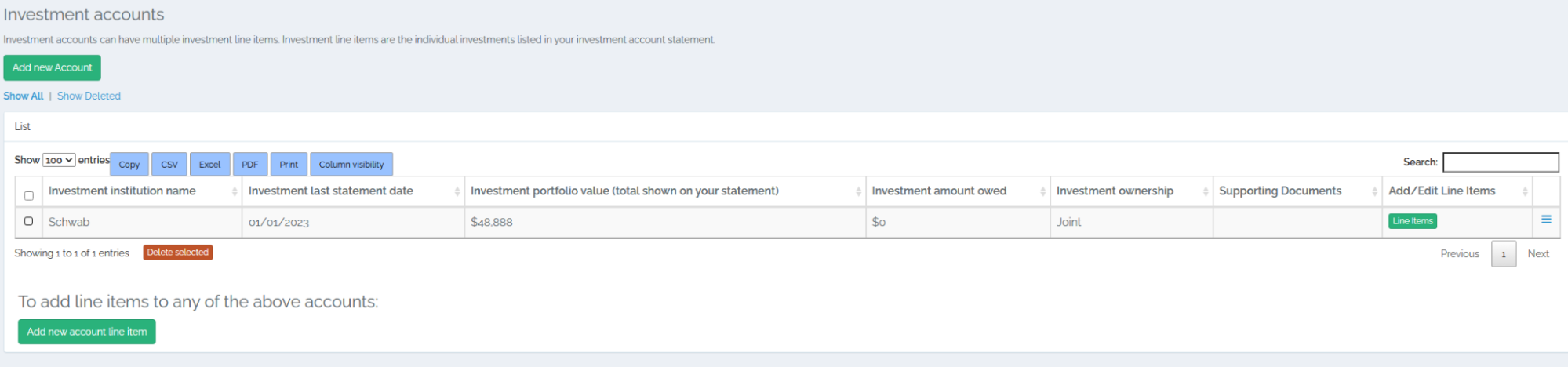

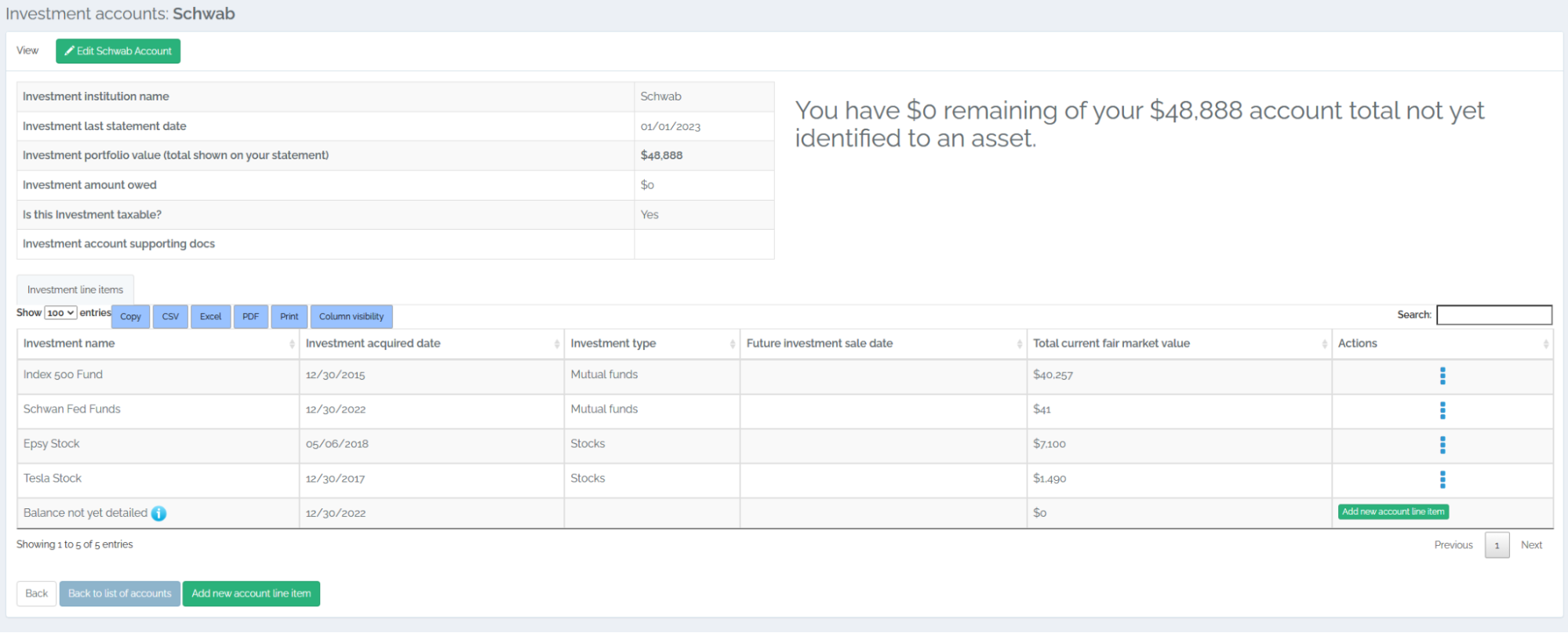

Investment accounts are typically held at financial institutions like Schwab, Vanguard, Fidelity, JP Morgan, and others who hold your investments in stocks, bonds, marketable securities, retirement accounts etc.

The tree methods of accounting for investments are Summary, Detailed and Hybrid.

1. Summary – The easiest

way is to show just the total value of your account at a specific date. This is

a great way to start off. It is easy to stay current by simply updating your

end of month total value. If the account is probably going to remain with you

or your spouse then its total value may be all that is needed.

2. Detailed – This method

requires you to enter each specific asset held in the account. It is the most

detailed and allows you to then split each individual investment asset to you

or your spouse. This will require additional time to update your account and

keep it current depending on the number of individual assets held in the

account.

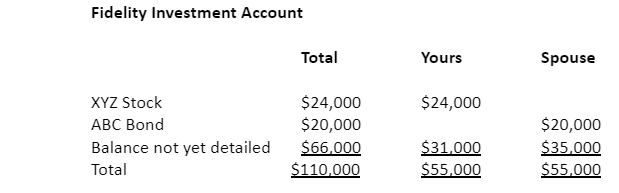

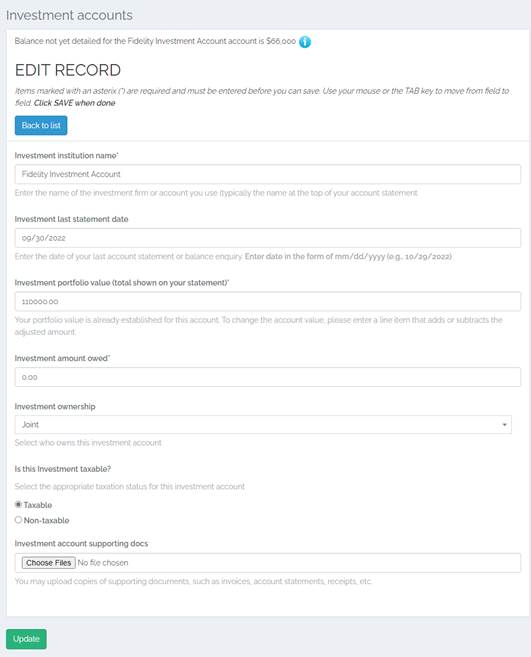

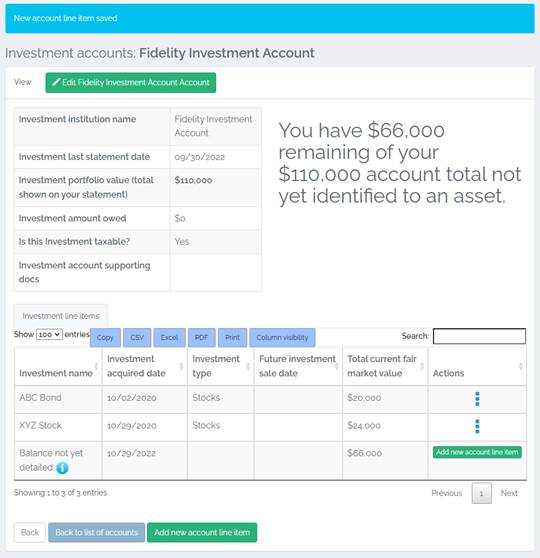

3. Hybrid – You start out with the Summary, and then list only those individual assets that you have identified are going to require specific allocation to you or your spouse. For example, the Fidelity Investment Account valued at $110,000 has XYZ Stock that you want, your spouse wants the ABC Bonds and the balance you will split to equalize the account split. You would enter the details for the XYZ Stock, the ABC Bonds and leave the remainder as “Balance not yet detailed”. Your goal is:

The Hybrid method would look like the following in D|S Investment Accounts:

In Divorce|Split you have three options to identify who owns a specific asset or debt. It will be Yours, Spouse’s or Joint. In special circumstances you may find it advantageous to split an asset into two parts and then assign ownership. For example, you own 200 shares of XYZ Stock. 100 Shares of XYZ Stock you owned prior to marriage and the remaining 100 Shares of XYZ Stock you jointly own. These could be split into XYZ-A which shows 100 shares owned by you, and XYZ-B which shows 100 shares jointly owned by you both.

SMS, or Short Message Service, is the protocol used by cellular phones to send and receive text messages over a 2G, 3G, 4G, or 5G network. Unlike app-based messaging services, you don't need a data plan to send and receive SMS.

We’re all familiar with SMS, or standard text messages. After all, it’s one of the oldest and most commonly used methods of mobile communication. While SMS is seemingly humdrum in the modern age, there’s a surprising amount of coordination and technology working in the background to send such seemingly simple messages.

Special adjustments are accounting cases where special considerations must be given to assets under specific circumstances and/or history. Examples are given below. These special adjustments should be discussed with your attorney as soon as possible to ensure that they are processed correctly, proper notice has been given, careful records and supporting documentation are preserved or acquired to ensure the special adjustment is accurate, complete, and allowed in arriving at your final equalization payment. These special adjustments are called:

Epstein

Watts

Moore-Marsden

CA Family Code 2640

Other

- Epstein – Typically we refer to “Epstein Credits” as a reimbursement to one spouse for paying after separation a community expense before the trial starts. For example, assume one spouse makes a mortgage payment of $2,600 on the couple’s community property residence. The paying spouse is entitled to one half or $1,300 from the other non-paying spouse. Careful records and documentation must be kept, to prove the source of funds used and the community expense paid.

- Watts – A Watts charge (or Watts Credit) arises when one spouse uses community assets after separation. A typical example would be where one spouse lives in the couple’s community property personal residence. The spouse living in the residence (in essence they own one half) can be charged one half the use (rental) value of the residence (for the other half which is owned by their spouse).

- Moore-Marsden – Is a formula that is used to calculate your and your spouse’s interest in real property where one spouse purchased the real property prior to the marriage. If this applies to you, consult your attorney. For further understanding of Moore-Marsden there are several articles on-line including Moore Marsden | Property Division (mesniklaw.com), Terrific Guide on Moore Marsden Law, Calculation and Examples For 2021 (farzadlaw.com), What is a “Moore/Marsden” calculation and how does that effect the division of community property? — San Diego Divorce Attorneys Blog — October 14, 2015

- CA Family Code 2640 – Typically this code section recognizes the need for recovering a down payment made from one spouse’s separate funds to purchase a home during the marriage. The code section includes down payments, payments for improvements and the principal portion reduction of loans to purchase or improve the property. However, it does not include any interest paid on loans or the usual ownership expenses like maintenance, repairs, property taxes, associations fees, utilities, insurance and the like. The amount of the down payments or other qualifying payments must be identified, documented, and separate source of funds must be clear and specifically identified as well.

- Other – This can be used to identify an amount not covered in one of the above and not included in the community property report. For example, a winning lottery ticket you just found out your spouse had purchase prior to separation. A gold coin just found, or your spouse’s paid divorce attorney retainer where your spouse hid the funds during the marriage and failed to disclose them as community property.

Split Scenarios allow you to allocate or split assets and liabilities (Debt) between you and your spouse to arrive at an equitable “property settlement”. It provides a comprehensive analysis of all aspects of an equitable split, including calculating the equalizing payment, if one is necessary, from you or your spouse to balance the split. Your subscription level determines how many different split scenarios you can create. Your subscription level also determines if the split scenario is simply an “Equity Split” or one that allows you to also see the “ATCV” (After Tax Cash Value) of your property split and therefore the tax implications of your split choices.

Like Investment Accounts methods of data input, the ATCV function can be “detailed” ie. used for all taxable assets or “hybrid” ie. simply limit it to the significant assets that upon sale have a material tax impact. This will help you negotiate an equitable property split and settlement.